Edmonton’s Latest Condo Fire Should have you Rethinking your Condo Insurance Plan

No matter how responsible you are, someone else’s mistake could cost you thousands if you don’t have the right insurance. That’s especially true when you live in a condominium.

The fire on Friday, May 22 that destroyed a 106-unit condo building in North Edmonton, caused an estimated $16.3 million in damage, the Edmonton Sun’s Claire Theobald reported. One unwitting resident who tossed a cigarette butt into a diaper container sparked this huge loss.

Although no one was injured, as many as 200 families and residents have been faced with the heartbreaking prospect of starting over. Our sympathies are with all these families as they prepare to enter this difficult and highly emotional time. And although I would like to hope otherwise, I am all too aware of the unfortunate financial position that some of these same residents will soon come find themselves in which is: the condo insurance they have been paying for is not going to come close to covering what they will need to shell out for living expenses over the next year or two.

Here are a few reasons why you should take this recent condo fire as a much-needed wake up call, and take some time to review your condo insurance plan with an insurance professional so that you can rest assured that you’ll be financially able to face the unexpected.

#1: If you own and are found guilty, you could be held responsible

If the resident who improperly discarded the cigarette butt is also the owner of his or her condo, the condo owners association could hold them liable for the damage. Personal liability protection is just one of many reasons why you want to have a solid condo insurance policy.

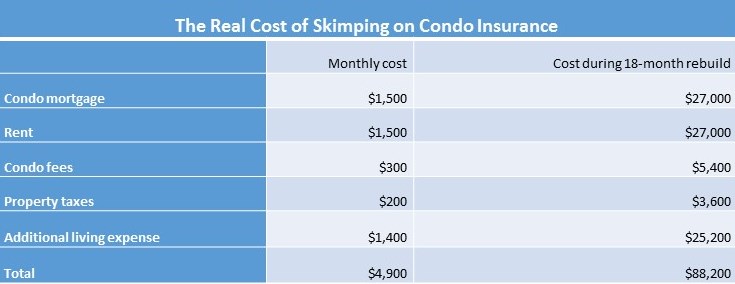

#2: During rebuild, you could pay up to $88,000 in living expenses

Global News says rebuilding the condo is expected to take a year and a half. What can you take away from this? Well, the fact is, even if you have the basic amount of condo insurance your lender requires, you may not have enough to cover your living expenses for 18 months in the event that your home is destroyed.

Also, things get stickier if you own your condo unit as you would still be responsible for mortgage payments and condo fees during rebuilding, even though you’re not living there.

Condo insurance will sometimes cover your condo fees if you don’t buy the cheapest policy available. And while condo insurance won’t cover your mortgage payments, it will cover any additional living expenses you incur while you wait for your residence to be restored.

A basic condo insurance policy might provide up to 50% of the personal property limit in addition to living expenses coverage, which means your personal property limit is very important. If it’s only $25,000, the most your policy will pay for additional living expenses is $12,500 which might not cover your rent for as long as it will take to rebuild. You might prefer to pay more for additional coverage.

#3: Personal property coverage protects your possessions & condo upgrades

Speaking of personal property, those Edmonton condo fire victims who went back to assess the damage the following week found their possessions ruined and water-soaked. In order to avoid replacing all your possessions following a disaster, you’ll definitely want personal property coverage to replace your furniture, clothes and other things. A condo owner’s policy also covers condo improvements and betterments — any upgrades to the unit that the condo owner paid for, like upgraded flooring, cabinets, and fixtures. The condo association’s insurance policy only covers damage to the basic building structure and common areas.

#4: Avoid paying out of pocket for loss assessments

A condo owner’s insurance policy also covers loss assessments. If there is a claim to the condo common areas, and the condo corporation wants the unit owners to take on a portion of the loss, insurance will provide coverage for this assessment if the claim was caused by a peril that is insured under the policy.

If you're renting out your condo, you will want to stipulate in the lease that the tenant is responsible for getting their own tenants insurance. The condo owner will have their own policy for the issues I just described, but the renter needs a policy to cover their liability as the tenant of the unit and to cover their personal contents inside the condo. The condo owner is still responsible as the owner for liability, condo improvements and betterments, loss assessment and the appliances in the unit.

If you’re unsure of how much coverage your current insurance policy offers you, I can review your existing insurance policy and your condo association’s insurance documents to see if you’re exposed to any unnecessary risk. Then I can help you get a quote for a condo insurance policy. When you have the right insurance, you can focus on the logistical and emotional aspects of recovering from a fire while the financial aspects are largely handled for you.

Featured photo: Courtesy of the Edmonton Sun

Sources:

https://ama.ab.ca/condo-insurance-coverage-options/

http://arcinsurance.ca/residential-insurance/condo-insurance/

OWN. GROW. PROTECT. First Foundation is the one-stop-shop for financially responsible Canadians looking to get great advice and save money. Whether arranging financing for a property you OWN, or looking…