Top 7 Things The Canadian Federal Budget of 2014 Says About Mortgages

Well Minister Flaherty announced the 2014 Canadian Budget and I thought I’d dig through it to find out what it said on the state of housing and the mortgage market in Canada.

Here are the top 7 key points I was able to decipher:

1. Residential housing is a big part of our economy and a key contributor to our economic recovery since 2008. (p.47)

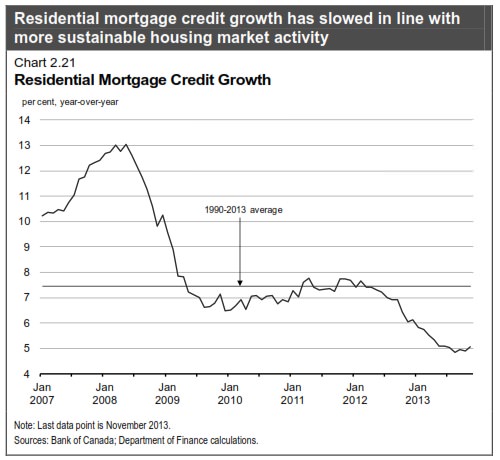

2. Mortgage rule changes implemented over the past number of years have been helpful in moderating housing activity and cooling mortgage credit growth. (See chart) (p.47-48)

3. Recent price increases in housing have largely been limited to Toronto and Vancouver and are not broad-based as they were prior to 2008. (p.47-48)

4. Recent changes have been effective but the Government continues to monitor the situation and will act further if it deems necessary. (p.47-48)

5. The goal of intervening in the housing / mortgage markets is to ensure disciplined lending practices and to reduce consumer exposure to the housing sector (i.e. Government-backed insurance losses). (p. 134 - 135)

6. The Government recognizes that Canadians benefit from competitive financial services and encourages such. Several new rules should help level the playing field for small banks and credit unions. (Incidentally, as mortgage brokers, we also believe Canadians benefit from competitive financial services)

7. The Government views collateral charge mortgages as a consumer awareness issue (comparable to payday loans) and intends to raise awareness about them and increase transparency requirements. (p. 195) (Talk to us if you have questions. It’s serious and you need to know)

Important Quotes

“Consistent with this moderation in housing activity, the growth in residential mortgage credit continued to cool.”

“Moreover, the most recent increase in housing activity and prices has not been accompanied by an acceleration in residential mortgage credit growth. This suggests that homebuyers are purchasing homes with larger down payments and that existing homeowners are taking advantage of low interest rates to pay off their mortgages at a faster rate.”

“The Government continues to implement measures to increase market discipline in residential lending and reduce taxpayer exposure to the housing sector.”

“The Government has adjusted the rules for government-backed mortgage insurance four times since 2008...”

“Canadians benefit from a competitive banking sector in which providers, in particular smaller banks and new entrants, compete for business.”

“The Government will continue to raise public awareness about the costs of and alternatives to payday lending and other high interest rate lending products, collateral charge mortgages, and bank powers of attorney and joint accounts.“ (emphasis added)

“While many consumers continue to choose a traditional mortgage to secure their home loans, many are increasingly choosing collateral charge mortgages. The impacts of having a collateral charge mortgage may differ from traditional mortgages. For instance, switching between lenders may be more difficult. To make an informed choice, consumers need sufficient information to clearly understand the costs and consequences of collateral charge mortgages relative to traditional mortgages. The Government will require enhanced disclosure, better equipping borrowers to understand these impacts.“ (emphasis added)

You can read the entire 2014 Canadian Federal Budget here:

President of First Foundation Residential Mortgages and First Foundation Insurance. Live in Edmonton but cheer for the Riders. I have lots of kids. Follow me on Twitter @gordmccallum